When applying for financial protection, many individuals are surprised to find that two people of the same age can pay vastly different amounts for the same policy. At Well Spring Insurance Benefits, we believe in transparency throughout the underwriting process. The two most significant factors that influence your monthly costs are your smoking status and your comprehensive health history.

Understanding how these variables interact can help you better prepare for your application and potentially secure more favorable rates.

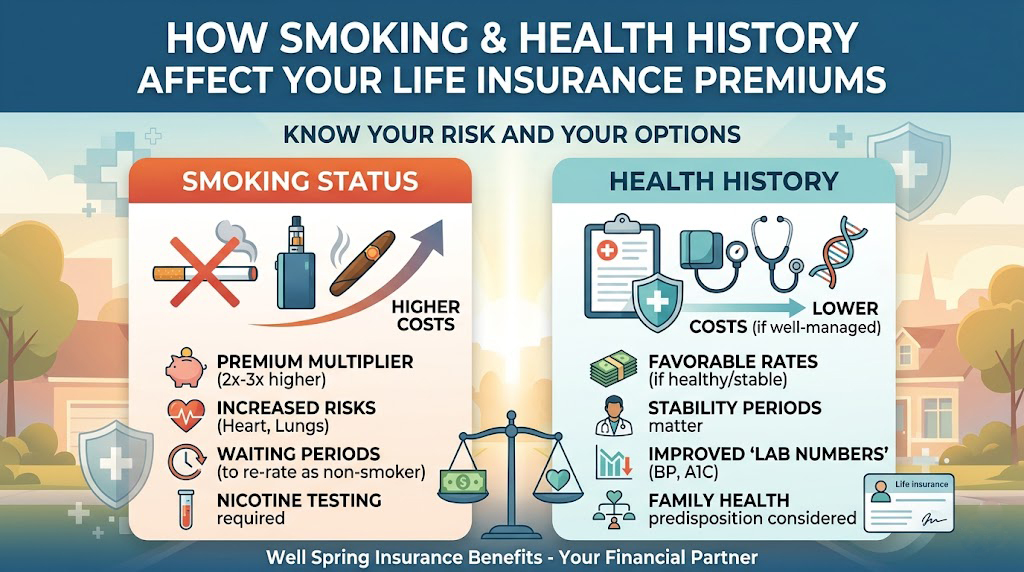

How Smoking Impacts Your Life Insurance Costs

It is no secret that tobacco use carries health risks, and insurance carriers reflect this risk through “Tobacco User” rate classes. On average, smokers pay 200% to 300% more for coverage than non-smokers.

What Counts as “Smoking” to an Insurer?

In 2026, the definition of a smoker has expanded beyond traditional cigarettes. Most carriers will classify you as a tobacco user if you have used any of the following in the last 12–24 months:

- Cigarettes and Cigars

- E-cigarettes and Vaping products

- Chewing tobacco or Nicotine patches/gum

- Pipes

The “Smoker” vs. “Non-Smoker” Rate Gap

Insurers typically offer four main health tiers. Smokers are almost always relegated to the “Tobacco” versions of these tiers, which carry a significantly higher base premium to account for the increased risk of respiratory and cardiovascular events.

Health History: The “Risk Map” for Underwriters

Beyond lifestyle choices, your medical background serves as a roadmap for an insurer to predict future mortality risk. When you apply for life insurance, underwriters look for patterns of stability and wellness.

Key Health Indicators Insurers Review:

- Cardiovascular Health: Blood pressure and cholesterol levels are primary indicators of heart health.

- Metabolic Health: A1C levels and blood sugar management for those with diabetes.

- Family History: Carriers look at the health of your parents and siblings to see if there is a genetic predisposition to certain cancers or heart disease.

- Body Mass Index (BMI): Your height-to-weight ratio is a standard metric used to categorize general physical health.

Comparison: Estimated Premium Impacts

The following table illustrates how different health and lifestyle factors can shift your premium “multiplier” compared to a standard, healthy non-smoker.

| Factor | Impact on Premium | Underwriting Note |

| Non-Smoker (Preferred) | Base Rate (1x) | Excellent health, no tobacco use. |

| Current Smoker | 2x – 3x Increase | Requires 12 months tobacco-free for re-rate. |

| High Blood Pressure (Controlled) | 1.1x – 1.2x Increase | Minimal impact if records show stability. |

| Type 2 Diabetes (Managed) | 1.5x – 2.5x Increase | Heavily dependent on A1C and age of onset. |

| History of Major Illness | Variable (Table Ratings) | May require a “waiting period” post-recovery. |

5 Ways to Lower Your Premiums

- Commit to a Cessation Program: Most insurance companies will allow you to apply for a rate reduction after you have been 100% tobacco-free for at least 12 to 24 months.

- Demonstrate Treatment Compliance: If you have a condition like high cholesterol, show the insurer that you are following your doctor’s orders and taking prescribed medications consistently.

- Improve Your “Lab Numbers”: Small improvements in your BMI or blood pressure in the months leading up to your exam can move you from a “Standard” to a “Preferred” rate class.

- Consider “No-Exam” Policies: If you have minor health issues, a simplified issue policy might offer a more favorable automated decision than a manual medical deep-dive.

- Work with an Independent Agent: At Well Spring Insurance Benefits, we shop multiple carriers because each company has its own “niche.” Some carriers are much more lenient toward occasional cigar smokers or managed diabetics than others.

FAQ’s

Can I lie about smoking on my application? No. Insurance companies test for nicotine and cotinine during the medical exam. If you are caught misrepresenting your status, it is considered insurance fraud, and the company can deny your claim or cancel your policy.

What if I quit smoking after I bought the policy? Many policies have a “re-entry” or “re-rating” option. Once you’ve been tobacco-free for a specific period (usually a year), you can request a new medical exam to move into a non-smoker rate class.

Does family history matter if I am perfectly healthy? It can. Some “Preferred Plus” ratings are only available if no immediate family members have passed away from heart disease or cancer before age 60.